Hi hope you see my comments have been missing a lot.

The last weekend was the theme of Greece so dominant and regular U-turns at Hilfszu and -Shaped cancel that the situation could have simply offered too many opportunities that I hardly had written my comment, already to stand like an idiot. And I will prefer to pick me for other occasions. Is already enough to give it. ;)

Have a couple of times cited the headline: "Greece Is Europe's Bear Stearns, But What Will Be Its Lehman" Maybe Greece Bear Stearns and Lehman is simultaneously or in succession. I do not know, was in the matter but ever optimistic. Big statement I want to make not. (Just this: I tend to lately, not Greek euro coins to spend more but to keep me in the Expectation that in future they might get even collector's value;.)

I think all this now but not quite as particularly important for financial markets. Greece, I see now that is not the cause for the current crisis, but only as a symptom, as well as the Thursday crash after an allegedly erroneous trade.

The real reason I see in the fading risk capital. And that in turn is a story that I've written frequently lately, namely the quantitative easing program of the Federal Reserve, or rather its end.

See if you please include the commentary from 5.4.

http://franzlischka.blogspot.com/2010/04/mein-ublicher-senf-zur-aktuellen.html (There is also the link to my previous comment from 7.3. In which I wrote about the slightly complex background a bit more).

Again, why is this rather dry subject of my opinion, maybe strength for the financial markets than what happens on the streets of Athens? It's simply about the dimensions. The aid program for Greece to € 110 billion to be difficult (or now, but 150?) And run over 3 years. (This is no new money to be created, but only borrowed money that Greece would have otherwise borrowed without a crisis in the financial markets themselves.)'s Largest (but not the only) sub-program of the QE of the Fed, however, the purchase of mortgage Backed Securities (MBS) for a period of 15 months in the amount of $ 1.25 trillion (!) Derived directly from the printing presses! This could be along with Greece, Portugal and Spain, probably Italy, fund out for a few years.

So now is the program (for now) and displays the history is much faster now than I ever thought about the markets. Here are the updates of the charts from 5.4.

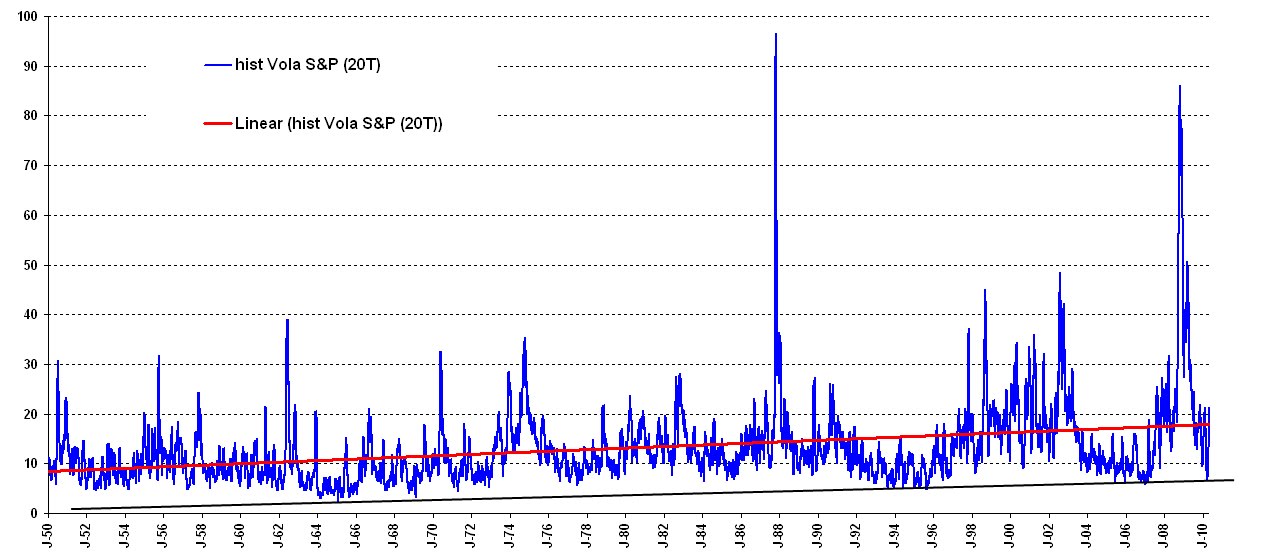

The impact on the volatility is huge. The downward trend in volatility has turned clear

Only recently, the realized volatility (Chart: S & P 500 20-day volatility since 1950) to historical low level dropped. And only 1 ½ years after the biggest financial crisis in 70 years. Chart: black the upward trend in the volatility since the end of the 2nd World War II is (why the upward trend is, I write is another time in detail), red linear regression over time. From far below-average volatility in early April, we are already above-average values:

With the palm turns almost any risk trade in the last 12 months.

Zb European Corporate Spreads:

is really interesting things when you then the relationship between the QE-dates and the crisis in the euro area is considered:

10-year government bond spreads of PIIGS countries to Germany, gecapt for readability at 6%. (Now the Greece-spread is already at over 9%)

The 1 QE-Programme was still no effect, with the 2nd marked but the spreads of Greece (red) and Ireland (orange) their tops. When the program ended, the new crisis began to escalate.

What is the message of this? Ultimately, all are

Risky Assets for the last 2 years only a single trade was. Either rose or fell anything everything. And it was all driven by the trillions from the printing presses of the Federal Reserve.

shares:

Commodities:

carry trades (Chart Australian Dollar):

emerging market currencies (Chart Brazil Real.)

So what I'm saying is, think I am clear that the whole risk trade was driven by money from the Fed, and this is now no reason to fear that everything will engage the reverse gear.

Yes, the economic data are currently excellent. Unfortunately, they were also the 2007 (and in many countries, even early 2008). Meaning, this has not necessarily mean much now. Finally, run ahead of the stock markets and the economic recovery was in general only by the boom in corporate bonds, etc. possible.

I see the strong data is a problem: The QE-end was like a huge increase in interest rates, but with an ISM of around 60 it is difficult for Bernanke, the soon to reverse, start to say his helicopter and re-bills to raise the already maligned bankers. Only when the U.S. should put the end of the year on the brink of recession and triftet inflation to zero (base effect driven and by lower commodity prices is very likely) ...

... and then when the markets re-lying on the floor, then Bernanke can start a new QE-Programme which is then likely to be even larger than the previous. Then it's time to buy stocks and Co, but until then, we should perhaps better hide under the covers. I think that is not a funny summer.

And also hope that China will save the world economically, I'd rather not share. Nearly 3 weeks after my last comment, broke through the Chinese stock market short-term upward trend, thus confirming the long-term downward trend. And having given a "Death Cross" (opposite of the "Golden Cross" 50-day line (red breaks) 200-day line (yellow) to bottom, a very very reliable trend indicator) was formed. See chart technically from real bad:

The negative here: the market is actually in the last few years, a precursor to the other markets have been (orange: China Mainland, green: MSCI World, blue: MSCI Emerging Markets):

seem short term, the markets now, but something about nervously, and perhaps come at the weekend now, but a clear signal from the EU to Greece & Co, but anwirft to Bernanke again the printing press is, for me the only question, then where the next crisis breaks.

Nevertheless much fun. ;)

LG

Franz

0 comments:

Post a Comment