Hello,

me now but surprisingly quickly grabbed the writing's content. But the weather is bad, and promise to stop the markets to be exciting. ;)

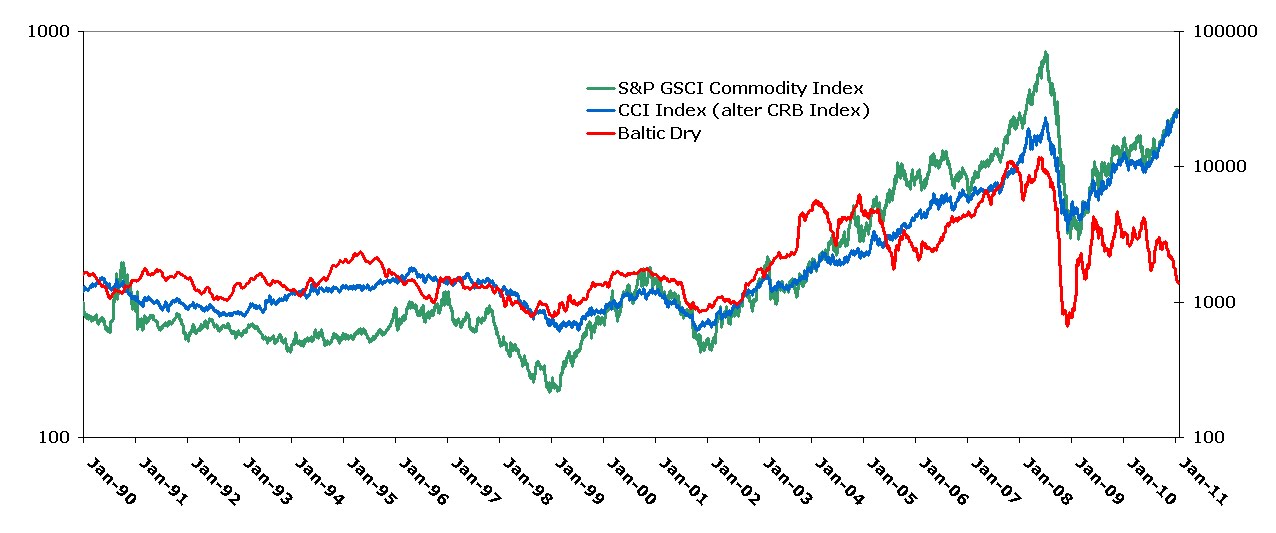

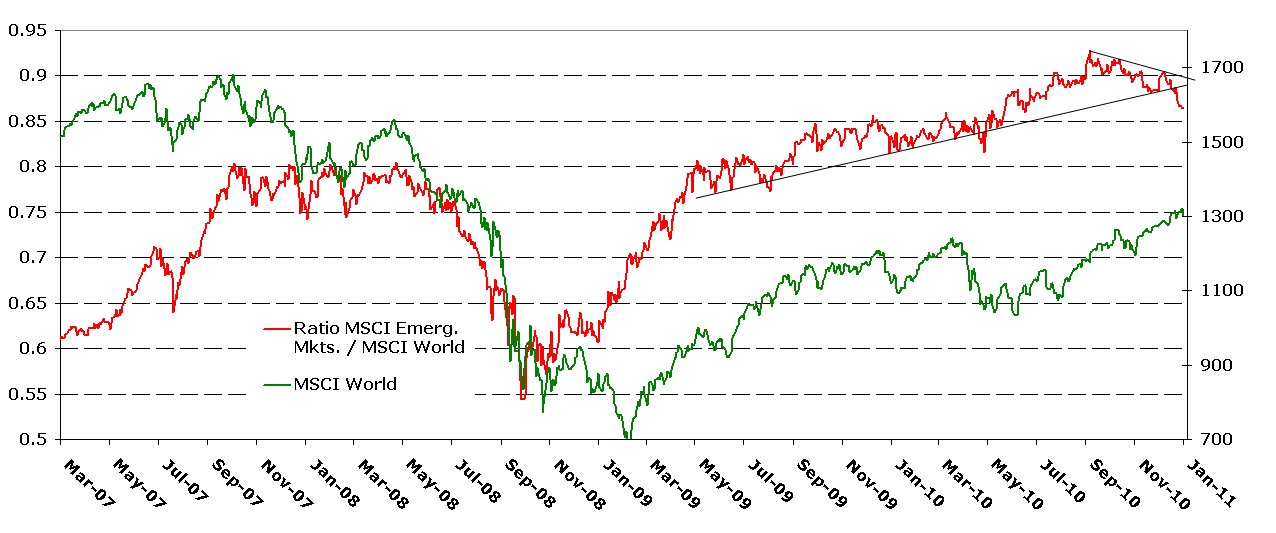

as an introduction to an update from the EM / DM (developed market) ratio as an early indicator of the global equity markets. Showed in the last week, while further down it came in the first EM ETF on Friday night in New York than all non-American markets had already closed, due to the escalation in Egypt only really for the sell-off. Will continue in the pace early in the week thus more likely. (And because I grade when updating last week's charts am: The Baltic Dry is broken by a further 17% I wonder when the first shipping company becomes insolvent.)

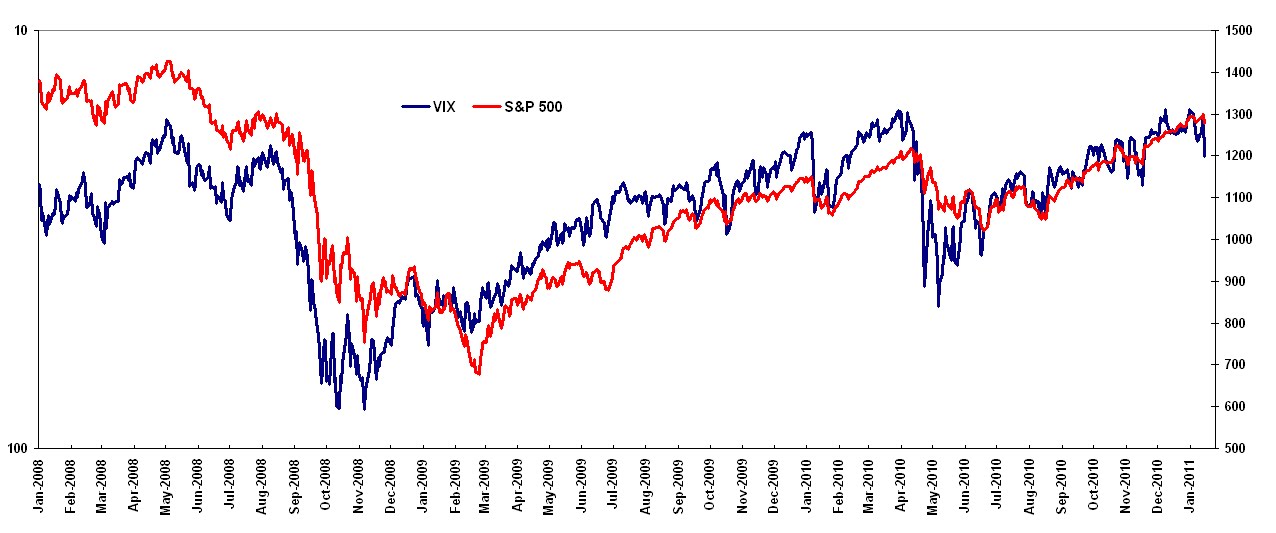

Friday night show but then the U.S. markets for the first time vulnerable . This looks best in the volatility. This was especially pleased with the turn of the year an incredible compression shown in the daily fluctuations. Actually, really unbelievable, but true: Only 2 years after the financial crisis that brought us tremendous volatility, was the volatility (measured by the change of the closing prices of the last 20 days) not only among the long-term upward trend (black) like that in April last year for a reversal of the volatility and thus led to a sharp correction in stock markets. No, the volatility was even now fallen to a level that was lower than that at the height of the credit bubbles of the last decade. In fact, it was even the lowest level since 1971!

(red: the regressed average trend line)

Even if the lies allegedly mainly to the high frequency traders who now make up the bulk of the trading volume on the NYSE and the driver has volatility-dampening (at least until they do not like the flash crash on May 6, suddenly out of the market pull back): In principle, a very low volume is a sign of too little anxiety and a contra indicator. According to the quote that sent me a reader once. "When the VIX is high, it's time to buy, when the VIX is low, it's time to go" The question is dependent, from where the VIX is high, from where low. Generally, you can quickly with such a tactic, of course, the falling knife attack. As in 2008, when many thought a VIX above 30, the market would be a clear buy and then had to watch in horror as he got over 80. I like the VIX as an indicator but because he often has a slight lead to the stock market. And there could now show an interesting situation: The VIX (blue, inverted, left logarithmic scale, S & P right scale) is now a part of course related to the historical volatility at very low levels and could the other hand, in recent weeks (low?) confirm the price rise in the S & P is no longer with a further decline. A turnaround is significantly more likely.

could also prove burdensome now the U.S. economy. Here there is indeed time being unclouded optimism. The ISM data from last month were in the sub-components very positive. In the weekly economic data, eg ICSC retail sales, mortgage applications and (in the chart below) Initial Claims (blue, right scale, inverted) is shown since the beginning but an end of the recovery.

no question that the bad data from the last week, in large part to weather conditions and will improve the next few weeks something. But the recovery trend in November and December is clearly broken. What surprises me not quite Finally, the recovery was indebted to a large part of the U.S. fiscal policy. In the fall should have the American people still expecting a massive increase in their tax burden of the year, when the so-called "Bush Tax Cuts" expire. Just in time for the for the so strongly consumer-driven U.S. economy is so extremely important Christmas business then the extension of tax cuts has been announced. The trade could then forward to the best holiday season for many years. But now, after the euphoria of the paint is starting slowly. The labor market data can further be desired. Consumers feel that they have no more money, but more than originally expected. And that's only for now. For while the federal government in Washington pushes the budget problems on the back burner, as the states of the water up to his neck. Illinois, the most severely stricken state, the credit default swap is traded for some time at a level between Iceland and Iraq, has just been raised dramatically in an attempted coup taxes. For the time being ridiculed by other governors, the example will soon become the norm. The giant state of California will soon adopt similar, does not want to go bankrupt. Even if fiscal policy by Washington to press the accelerator at the regional level there is only wailing and gnashing of teeth. And raises consumer sentiment not exactly.

yet another story that fits well into the picture:

A chart from the end of August last year, when the sentiment was extremely negative on the stock markets and was expected with a possible recession. At that time, in countless articles pointed out the seasonally unfavorable of September would be. At the time was then this year proved to be wrong. How often, if all expected. Is completely ignored, however, now that February is also historically a very bad month (and thus the large anomaly in the otherwise positive winter half year between November and April).

In sum then: The signs of greater Correction in equity markets take the last few days to clear. I now speak quite explicitly of stock markets, no longer on risky assets in general. What I have now but would exclude the time being that is, are the primary markets. In recent days, the political risk is now increased significantly and this could be the first time since the financial crisis lead to a splintering of the performance of stock and commodity markets. Now is not my main scenario, but in my opinion, underestimated risk. What if the protests spread (and, ultimately, one could almost say the "revolution") of Tunisia not only in Egypt but also in Saudi Arabia would? An oil price of $ 150 or more would be conceivable at any time. That would indeed be very negative impact on the economy. Would a scenario probably along the lines of 2008: Only a huge price increase and then a recession-related slump through the floor. In fact my total year-end forecast from last week would remain unchanged (ie negative). In the short term but I would conclude on raw materials for the time being no bet. Unclear to me would be the situation.

And so once again, until next time!

Greetings

Franz