Hi, I'm

for my first comment in the new year once again a few weeks left. Hope it's not why you become boring. ;)

But the very first weeks show surprisingly often the tendency for the remaining year. Although controversial, I see the so-called "January effect" as very useful. Especially the first two weeks to give the S & P 500 since 1950 in ¾ of cases the direction for the rest of the year. And that would be positive.

this I am but for now the positive messages. ;) The right on the most popular site in equity markets, the "most crowded trade" these days shows are now very massive weaknesses, namely in the emerging markets.

Did it already on 11 December last year, noted:

http://franzlischka.blogspot.com/2010/12/mein-ublicher-senf-zur-aktuellen.html (former trendline now located below dashed lines. Instead, as then, the outperformance I use now in order to improve traceability of the ratio, the not from the start time dependent. chart is exactly the same, but the scale is different.)

was the end of it then, probably "window-dressing" conditional, or by money from the retail sector, which is also momentumsgetrieben strong, short-term to a recovery. The market seemed to possibly on a new less steep upward move. Have therefore decided then, the issue of Emerging Markets from my outlook to To delete me because the situation was too uncertain. Well, last week the new uptrend has been broken completely clear, the short-term downtrend since October so clearly confirmed.

Again, the long-term chart. The double top from 1994 proved to be insurmountable for the time being resistance. Interesting that a ratio allows more significant technical chart points.

Reminder: This is the ratio (= outperformance) of the emerging markets to the "developed" countries. In absolute terms, the performance seen last week, but also badly bruised. Here, the MSCI EM in the form of the main index tracker the listed on the NYSE (ticker EEM). This shows now a fraction of the ongoing since the financial crisis uptrend:

Just last week I have some events again witnessed live and uninterrupted bullish regarding the sentiment EM, and how really "crowded" this trade is. If it still will break a trend that is for me a real game-changer. The correction, which I expect this could be very clear. And it will then show an impact on all other markets. After all, there were

yes, emerging markets, which the Western world in the financial crisis both in the crash, as were also in the recovery ahead. And not vice versa.

Far many years is the not entirely unexpected connection with the raw materials.

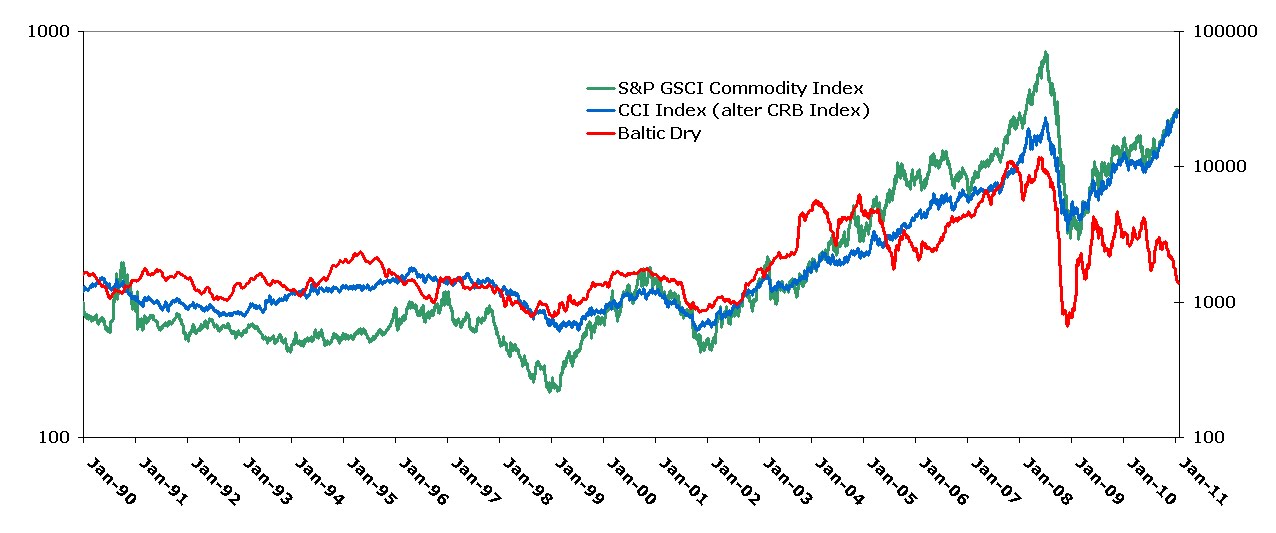

go Here I clearly believe that we will see this year with a correction of EMs is also a clear resetting of raw materials. (So I've been my outlook more pessimistic become the raw materials.) Green: the high oil-heavy S & P GSCI, blue the heavily agricultural-heavy Continuous Commodity Index (the further projected Reuters / Jefferies CRB Index in its former composition).

In this context, an update of the Baltic Dry Charts 19.12. The Baltic Dry compared with the raw materials. This time, however, even in long-term chart.

As can be seen, keeps the crash in the Baltic Dry continues. But is currently ignored. Argument as to why the index would not say more is on the cause of the crash. Unlike the financial crisis, it is not the sudden decline on the demand side, particularly the oversupply. In the boom years before the crisis, the construction of a vast number of cargo vessels has been commissioned, which are now completed. The decline shows that is not a weakening economy, but "only" massive over-capacity. Uh, hello? Is this not exactly the big problem of the emerging markets, especially China? It's all right, short-term is such a dramatic increase in capacity such as shipbuilding and in fact have been seen in the Chinese steel and cement industries still present in far more dramatic scale, positive for economic growth. But there comes the day of reckoning. A few days ago the largest shipbuilder in Vietnam went bankrupt, threatening the whole country once already celebrated as the new China, plunging into the crisis. Some are already seeing a new Asian crisis, which starts out in Vietnam. (Yes, the country is very small, but finally took the dramatic Asian crisis of 1997-98 also began in the economically second-Thailand.)'m Not sure about whether I would like to join this opinion. That in the next 10 years to a serious crisis in China is, I am convinced. Whether it actually happens soon, I'm unclear. In any case, I reckon, as I said, now even with a sharp correction in the EM exchanges. Perhaps the clearest

and how I see most controversial statement of my outlook was that we will see again this year a good retirement year. The first weeks were admittedly not in that direction. The weakness of the emerging markets and in my opinion, to increase following weakness in commodity markets, but now the chance that I get it right and the long-term downward trend in yields this year will continue. Finally, the current fear of inflation in the Western world is raw material for the time being driven almost exclusively.

A bullish development in the risky asset side I see it these days but still, namely in the PIIGS crisis. Very positive, I see that will be discussed more clearly on a debt restructuring Greece (which I think is inevitable), while the English spread does not shoot into the stratosphere, but falls to its lowest level in two months. Here is reaching from the market view that, while Greece, defaulter will most likely also Portugal and Ireland also likely that Spain but in a entirely different constitution. For the euro zone, the whole development would be quite a blessing. The 3 small PIIGS countries would default on their debts. This will avoid future moral hazard, without causing an excessive Lehman Meltdown in financial markets would, as it would in the event of a major country like Spain. I see the development in a long time for the first time back as positive. For the euro and equity markets in the medium term I would have voted positively. Relatively speaking, I think the future is EuroStoxx50 outperformed the DAX. (Taking into account the dividends; DAX is a total return index, Euro Stoxx 50, a price index), the German economy is however, very strongly to the demand for capital goods from emerging markets. Given the already existing excess capacity in China in my opinion, not an ideal condition for this decade, even if things work wonderfully.

Thus, in sum as an extension of my then still somewhat lean years outlook:

- Emerging Markets, the seller of the year 2010, will underperform

- raw materials are disappointed (so a correction to my old forecast)

- EuroStoxx50 proposes DAX

- Pensions: forecast largely unchanged: U.S. Treasuries will perform positive (and partly by the crisis in municipal bonds), it becomes a new QE-Programme after the expiry of the old end of June, come; Bund future but can suffer under the temporary relaxation of PIIGS crisis, English, Italian, Belgian, German, etc. Bonds are likely to outperform

And so until next time!

Greetings

Franz

0 comments:

Post a Comment