Hi,

as your notes, I've become lately read much lazier. I hope you read all the more attentive the few comments I read lately.

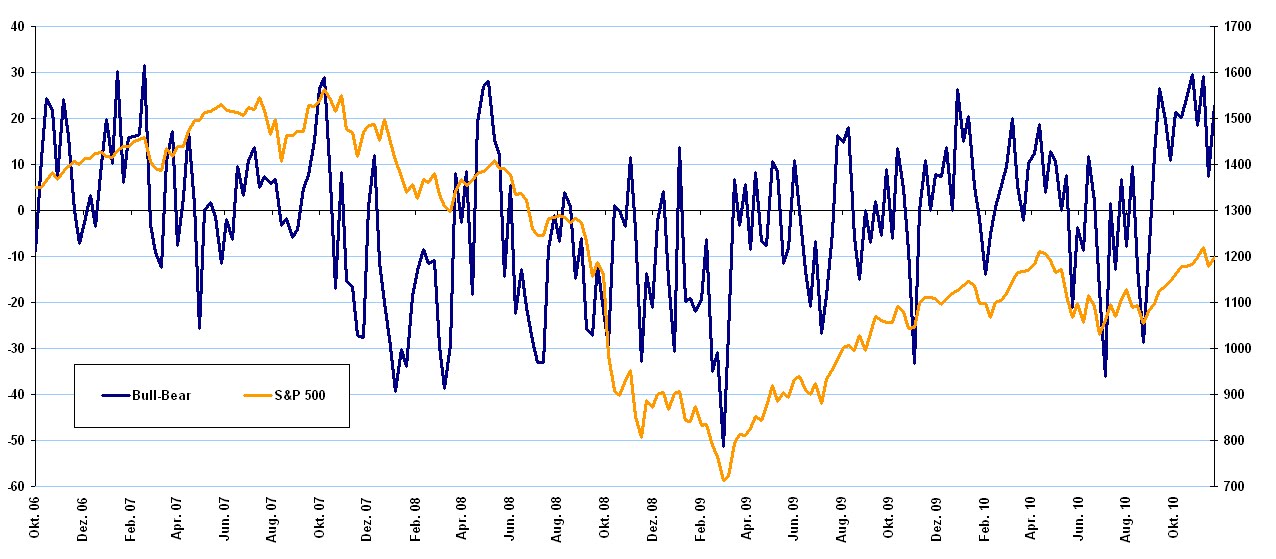

PIIGS The crisis seems like the last comment is concerned, to escalate. And faster than I would have thought. That the effect of the proposed rescue package to the Ireland markets fizzled out so quickly is frightening. If Spain should now tilt, the game appears to be off. In contrast to Ireland and Portugal, it would be for a Rescue probably too large. To do it yet, you have missed any powder. The targeted € 750 billion in May, although designed so that Spain is just starting. But then the crisis that ends exactly at where the politics out of money, is surely hard unlikely. And then it becomes dangerous to the markets. December is indeed historically anything but a crash month, and even a few days ago I would have thought that, accordingly, would escalate the situation until after the year, but maybe this year after a sensational September and October (the classic crisis months) this time anyway everything else. Optimism is in the light of the crisis potential in any case still very high, probably too high (weekly AAII sentiment survey of U.S. retail investors, the difference between "bulls" and "Bear"):

Since the announcement of the new QE-Programme of the Fed now several weeks have flown by. Time to first take stock. And there seems to Bernanke's washed to inflate stock prices and other risky assets, after a seemingly brief success but not to work. Instead, the situation seems to be what I've written a couple of times (eg at 29.8:. http://franzlischka.blogspot.com/2010/08/mein-ublicher-senf-zur-aktuellen_29.html , there are also links to my earlier QE-comment): For an inflation of Risky Assets purchased Bernanke simply take the wrong stuff, that is "safe" as once Satatsanleihen "risky" MBS. Here is an update of the MBS spreads (so that market that has been manipulated mainly by the 1st QE-Programme). The MBS spreads rise lately to new yearly highs. (Green: those decisions that led to a compression of spreads, red: those which led to a widening of spreads)

This also affects the stock market from:

interesting (or scary) again as in previous comments by the QE-related with €-government spreads (both 10-year government bonds, spread to Germany):

in the quantitative easing more than experienced Bank of Japan in their last meeting the purchase of corporate bonds and equities (using ETFs) decided. At some point, Bernanke will likely follow suit. Until then, his desire for asset price inflation will rise but not well-being.

As for the economic data, sees the camp in the U.S. are very different. Very strong Philly Fed, but catastrophic Empire State Manufacturing index, a very positive initial claims, but atrocious Durable Goods Orders, and a further weak housing market. The last few weeks provided very strong swings in the data, but in both directions. Let's see what brings the ISM on Wednesday. For me the most important indicator, but I look as ever more on the sub-indicators as the headline. (Data's on www.ism.ws) The further development in the PIIGS crisis is likely in the near future but superimpose anything anyway.

So until next time

Greetings

Franz

0 comments:

Post a Comment