Hi, this time after only one exception, again Week. Well, winter is approaching obvious when one looks at the weather Sun Given the increasing desire to write again.

The events of last week, I quote my last comment (below the AAII sentiment indicator, which showed an extremely bearish sentiment): "At this level, this is more of a clear bullish signal. As negative

I am in principle to the markets in the short term there is a clear short squeeze is possible ... "

And that hits the nail on the head. I read regularly these days that the data for the last week have dispelled fears of a new recession. "Is the double dip dead?" Was one of the headlines.

Complete Bullsh **!

As will be mentioned briefly, was nothing good. There are simply too many bets that the results turn out hard and they have just not on the scale. And there were too many short, they had to stock up again. Quote from last week regarding the news of the Hindenburg Omen ". On the other hand has just leave the intensive reporting on the mood of fall on such a negative level, that an immediate crash is unlikely," If too many are short, there is no crash no matter what happens. The best example was the Lehman collapse, happened after the end of September for the first time in almost nothing. I can still remember. On Sunday, Lehman went bankrupt, on Monday the sagging prices decrease, but on Friday already anywhere from a relief rally was mentioned. The S & P ended the week at that time have been positive. The crash came only three weeks later, after the mood had again become quite bullish.

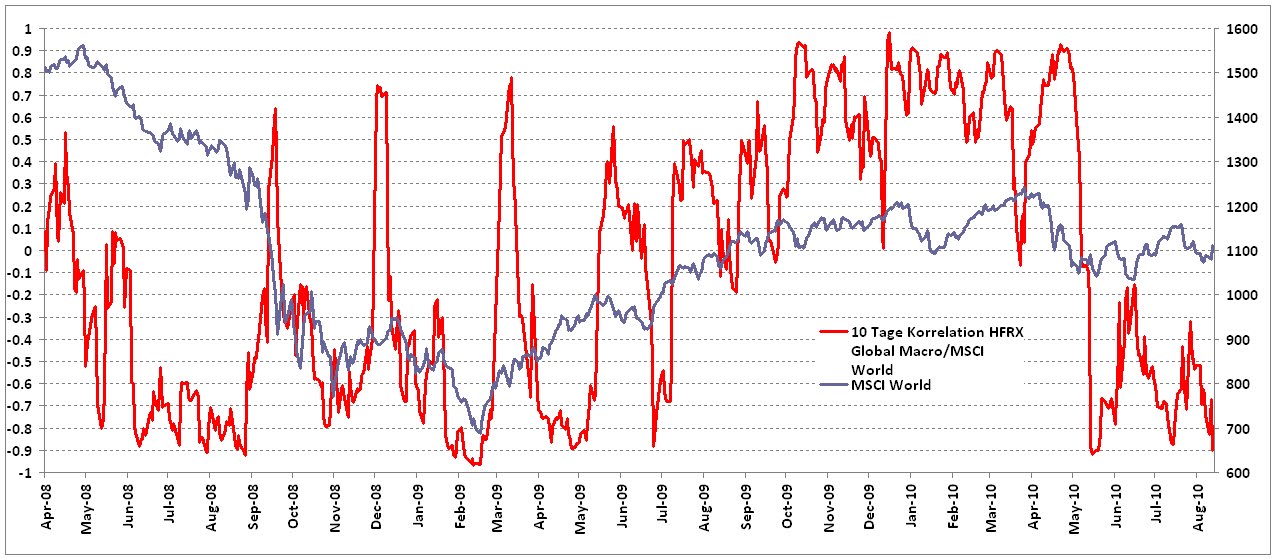

positions of the macro hedge fund based on the correlation to the MSCI World (Update of the chart from 19.6.): Goods this week so short as never before. Ouch, that has wiedermal hurt!

The mood this week, I think particularly of the Non-Farm Payrolls on Friday. Were these good numbers? Rubbish! Tends to be worse than last month and then prices fell because they were disappointing. This time, prices rise, although the data were poor, containing only the better than expected. It's all a question of Erartungen - and market positioning. And the numbers themselves: +67,000 in the private sector due to population growth in the U.S. far too little to keep the employment rate only constant. This would require well over 100,000.

But the most important figures for the month changes for me are always the ISM data. These were also the main reason for the rally. They were at first too strong. A rise in the headline number (PMI) instead of an expected significant decline. But a look at the details already looks less out favorably. From the ISM website ( www.ism.ws ):

The 3rd Consecutive increase in the two storage components (Inventories and Customers' Inventories), but also by 3 Consecutive decline in the two preceding components, the new orders and backlog (New Orders and Backlog of Orders):

Especially the latter is the fatal: The orders to hold it for long with the growth of U.S. industry with. I do not know if it's the strange scaling of the ISM data, or to the fundamentally optimistic attitude of Americans, but the ISM New Order component is almost always (more precisely 80% of the time) about the PMI and promises to even faster growth. (The Inventories component is historically interesting as it almost always under the PMI). Now that is not currently clearly the case, even worse, the difference (blue line, right scale) is -3.2 fallen to a level since the late 60's moved every time a recession by itself:

Although the time series is very volatile, so an eruption is already worrying.

And Non-Manufacturing ISM I do not need to say much. Significantly worse than last month and significantly worse than expected, but on Friday afternoon, the mood was far too good that the more someone has bothered much.

Thus, in sum: The catastrophe was avoided, but the trend is still downward trend ever. A recession has not been confirmed this week though, but was initially only postponed, not canceled. Shortly

to seasonality: in the historically weak period of 20 August to 31 September puncture the first 3 days of September than for this time of year produced an unusually positive. What I will say this: At the September-historically very negative seasonality changes, a good month starting one bit right.

A few words to the raw materials: copper remains very positive surprise, but the annual rate still generate a positive economic signal:

weak, however, the Oil price (blue): Did after the break of the uptrend in May established a new short-term upward trend, this in turn broke in August and win back in the strong rally in the risk assets last week, not again. Same time, the contango and therefore the rolling costs (red line, left scale) again significantly. Both are very negative.

addition, the seasonally strong period for crude oil is slow to end. (The seasonality in the oil price I think is one of the biggest misconceptions about the financial markets. Contrary to popular belief, the oil price in the summer is strong, weak in winter. The fuel consumption during the U.S. driving Season might be more influential than the fuel oil consumption in winter. Or maybe it is due to the Hurricansaison in the Gulf of Mexico. Or what ever ...) From www.seasonalcharts.de :

The oil inventory levels for this time of year to extreme proportions. Weekly report from the U.S. Department of Energy: http://tonto.eia.doe.gov/oog/info/twip/twip_crude.html # stocks (see chart U.S. Crude Oil Stocks in the left center of the page)

If in any case no Hurricane longer march through the oil rigs in the Gulf, the picture for the price of oil is increasingly negative.

And so until the next Time!

Greetings

Franz

0 comments:

Post a Comment