Hi sign me back wiedermal.

second Factors were the ones which, since 1 December the risk trades again given strong impetus to the market and gave hope to a year-end rally, and it sent the bond markets into a tailspin. The ISM - for me the most important economic indicator - was sometimes not, its subcomponents again significantly less favorable failed. (Again bearish New orders growth and inventories component at highest level since 1984). But the ECB

attacked deep into the wallet and bought between 1 and 3 December massively in the bond markets of the peripheral countries. This week pulled the spreads of the PIIGS countries but recovered to clear. The ECB has bought the politicians now time, but nothing more. The crisis is gone from the headlines, but in the next few months or even weeks, everything is probably high boil again. The only question is when.

The surprise of the previous week came from the U.S., and the politicians demonstrated clearly how the political divide between democratic president and overcome Republican House of Representatives Budget Questions: Everyone gets everything he wanted and this one has openly thrown in an incredible pace for all remaining congressional election in early November promises made to the fiscal adjustment over the side. If the Fed does with its quantitative easing program, already 70% of new debt, then you have less fear that you can not get the bonds at the man. The positive thing is of course that it has decreased the likelihood of a new recession in the next few years. Instead, shifts the problem again later. Surprisingly, in which more than generous deal was then, however, that the Build America Bonds program with 31 December will expire. This was with money from Washington subsidizes economic programs in the states. Are in fact primarily a bailout of those hidden states, such as the California, Illinois and New York on the verge of bankruptcy. The Republicans, the program was a thorn in the eye. Many of them wants a default of these states, since then the union officials' contracts expire. The market sentiment is still for the time being relaxed. One opinion I heard this week about a High Yield Manager, the consequences of such defaults, was: "Can I tell you now. If none of our crisis scenarios. In U.S. history is never a state defaultet. They get a safe bail-out. "Hmm, particularly the last sentence reminds me a little of what I heard earlier this year got to Greece. We'll see.

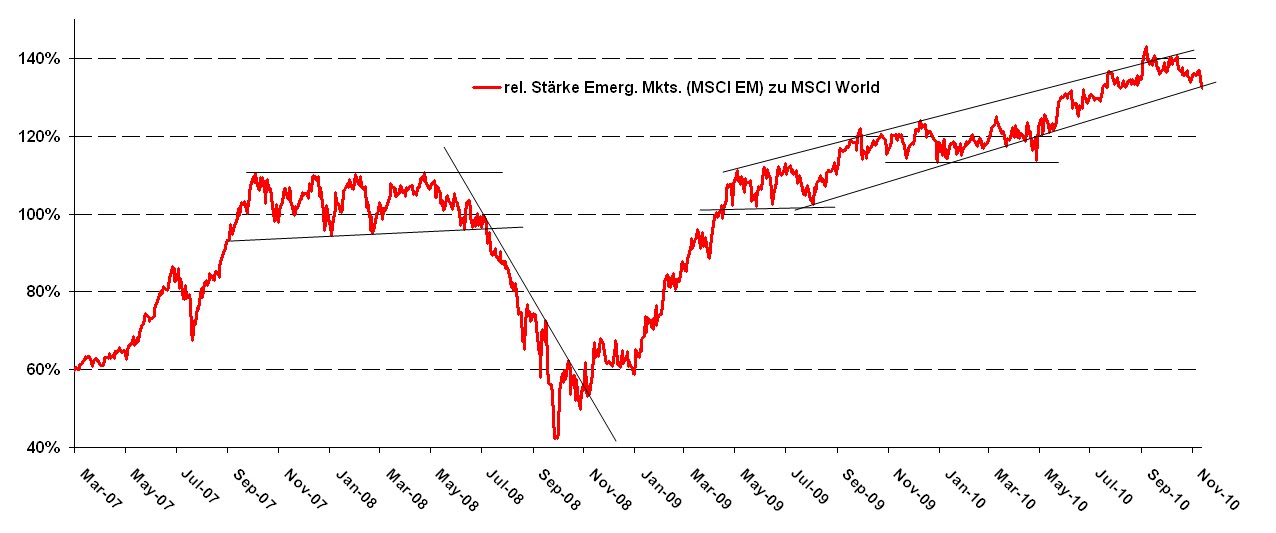

Sun, so it's time for a little picture, so it does not get too boring. And since I have a chart that concerns me grad. Maybe it has to mean nothing more, and the price movement is not too large. But it is at least surprising and it reminds me a little of a development in August 2008. And although it is about the fashion theme par excellence in the financial markets: the Emerging Markets (hereinafter often abbreviated EMs). If you believe the mood, they are the panacea for investors. High growth, little debt. Nothing else is currently sold anywhere near as good as the emerging market story. Well, what surprised me something now, is that despite the alleged massive inflows in this sector and despite the general risk on mood in recent months, the shares of these countries (as measured by the MSCI Emerging Markets Index) since early October after the clear developed countries (as measured by the MSCI World) back behind. (Rising line = EMs perform better than the MSCI World) Chart outperformance of emerging markets

The same chart since 1990. After the emerging markets, the relative offset losses since the Tequila crisis in Mexico in 1995 and the Asian crisis of the late 90's had the momentum was suddenly out of the market:

My Favorite Chart Analyst Chris Kimble has until Friday a Anaylse the most important markets in the emerging markets posted (Chart top center in the lower Tableu: the ETF on the broad MSCI EM According to Kimble potential SKS-Formation):

http://blog.kimblechartingsolutions.com/2010/12/falling-brics/

All concerns me despite the still very modest growth of why so much because the EMs in the recent years were the precursors for the Western stock markets often and not vice versa. The clearest I have yet to develop in August 2008 in the head as the EMs (then loved me hot with the argument that there indeed was no banking crisis) suddenly plummeting against the market sentiment. 2 months later, the Western economies went into the knee.

The relative price performance has been as I said, admittedly not very dramatic. But it is not just as one would expect (other than May, when the chart had given the former risk aversion as a result of a non-Greek crisis unexpected kink). are fundamental for the development of course it already: The food inflation, monetary policy in those countries are increasingly restrictive and that is not good for the capital markets. (This also parallels with 2008: Even then, the monetary policy of the EMs in a row, a dramatic rise in food prices had become very restrictive).

short term, the year-end rally seems increasingly endangered. The S & P has finally break the 61.8% Fibonacci retracement line overcome, where he had been frustrated. Spain, the crisis now cook up before year-end, we should be in the final weeks of the year, the historically by far the best time of year (Saisonaltiätscharts: http://www.seasonalcharts.de/classics_dj_ia.html ), higher stock prices . see

But I would keep an eye on emerging markets. Should stop the weakness could be a negative sign for 2011.

And so again until next time!

Greetings

Franz

0 comments:

Post a Comment